Most wealth management firms and family offices are not suffering from a lack of data. They are suffering from too much of the wrong data, processed too slowly, delivered too late, and trusted too little. The solution is not bigger data pipes — it is smarter ones.

The Wealth Management Data Problem Nobody Is Talking About Honestly

Walk into the technology strategy meeting of almost any mid-to-large wealth management firm today and you will hear the same word repeated like a mantra: data. More data. Better data. Faster data. AI-powered data. The consensus is that data is the competitive advantage of the decade — and that the firm with the most of it, processed by the most sophisticated models, will win.

There is enough truth in that premise to make it dangerous.

Because the part of the sentence that gets dropped — the part that determines whether that data investment delivers real returns or just expensive infrastructure — is the word that comes between “more” and “data.” That word is quality.

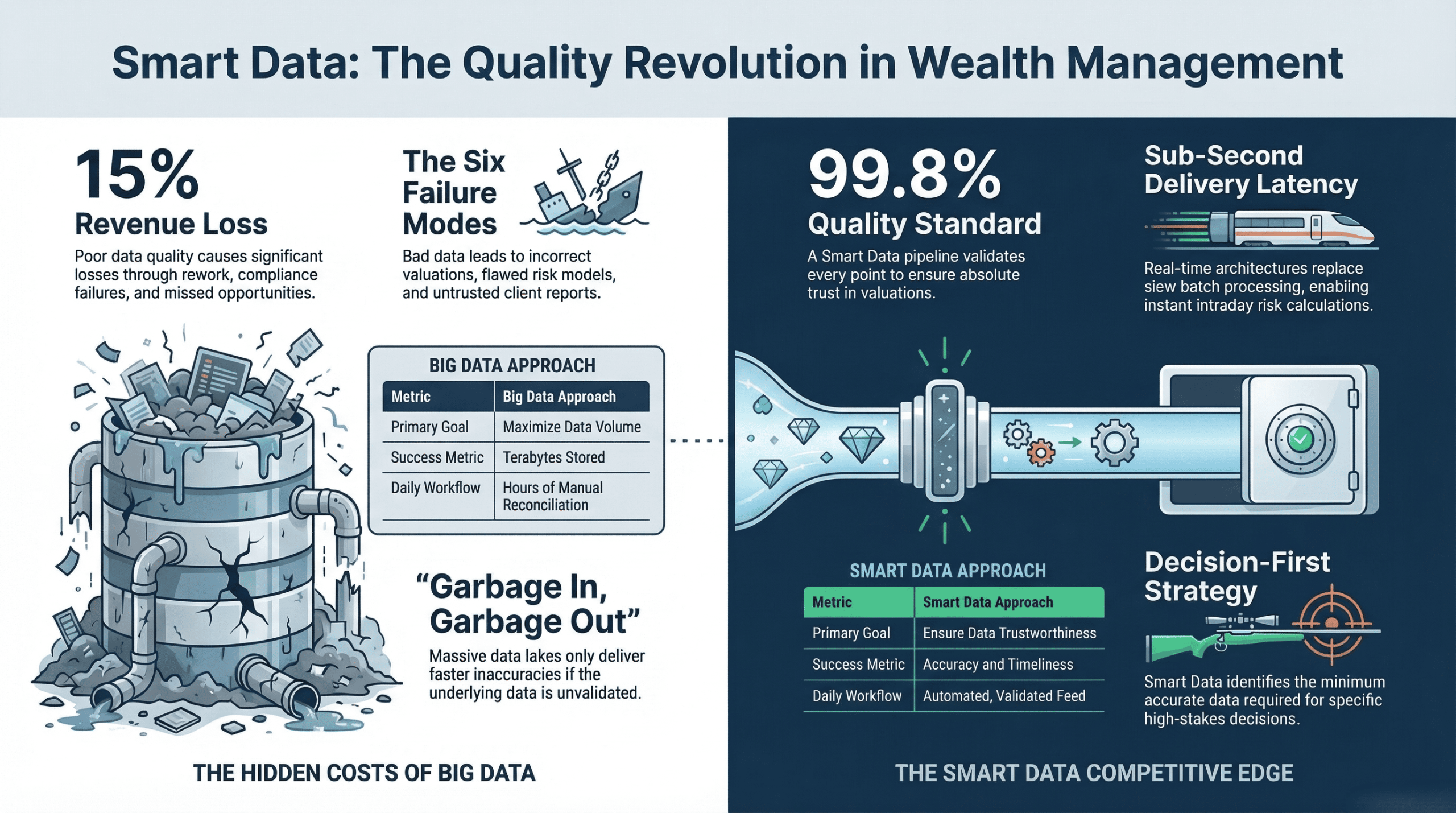

Across the wealth management industry right now, firms are investing in data infrastructure at record rates. A recent industry report found that 59% of asset and wealth managers are either adopting or considering Big Data analytics for investment operations. Data management is the most widely cited area for potential outsourcing among asset managers, with nearly half considering it. The investment is real, the intent is genuine — and the results are too often disappointing.

The reason is almost always the same. Firms are solving for volume when the problem is quality. They are building bigger silos when the problem is fragmentation. They are processing more data when the problem is that the data they already have cannot be trusted.

This is the distinction between Big Data and Smart Data — and understanding it is the most important data decision a wealth management firm or family office can make right now.

What Big Data Actually Means — and Why It Is Not Enough

Big Data refers to data sets so large and complex that traditional processing tools cannot handle them effectively. In the wealth management context, Big Data infrastructure typically means centralised data warehouses or data lakes designed to ingest enormous volumes of structured and unstructured data — market prices, transaction records, client data, economic indicators, news feeds, social media signals, ESG scores, and alternative data sets — and store them for analysis.

The Big Data promise is compelling: if you have access to more information than your competitors, and the computational power to analyse it, you will make better investment decisions, identify risks faster, and serve clients more precisely. In theory, this is true. In practice, the execution fails at a step that most technology vendors consistently understate: the quality of the data going into those systems.

When a wealth management firm builds a Big Data infrastructure without first addressing data quality, it does not get better insights. It gets faster delivery of the same inaccuracies that were already causing problems. It gets more comprehensive reporting of information that cannot be trusted. It gets an AI model trained on data that was wrong to begin with — producing conclusions that are confidently, systematically wrong.

Garbage in, garbage out. It is the oldest principle in computing, and Big Data investments do not change it. They just make it more expensive.

The Six Ways Bad Data Is Damaging Wealth Management Operations Right Now

This is not a theoretical problem. Bad data quality causes specific, measurable damage to wealth management firms every day. Here are the six most common failure modes.

Incorrect Portfolio Valuations

When pricing data is stale, duplicated, or sourced from conflicting vendors without reconciliation, portfolio valuations are wrong. Advisors present clients with net asset values that do not reflect reality.

Flawed Risk Calculations

Risk models are only as good as the data fed into them. An intraday VaR calculation built on incomplete position data or mis-classified asset classes is not risk management — it is risk theatre.

Compliance Failures

Regulatory reporting depends on accurate, complete, and timely data. Poor data quality in compliance functions is not just operationally costly — it is a regulatory liability that can result in fines and reputational damage.

Client Reports That Can’t Be Trusted

When a client receives a report containing errors their own team catches before you do, the damage to the advisory relationship is disproportionate to the technical error. Reporting quality is a direct proxy for perceived competence.

Operational Rework Costs

Every reconciliation break and every “that looks wrong, can someone check it?” moment is a direct cost of poor data quality. Research suggests firms spend 15–25% of operating revenue on rework driven by data errors — costs that are almost entirely avoidable.

AI That Makes Confident Wrong Decisions

As firms layer AI onto their data infrastructure, poor underlying data quality produces a dangerous outcome — AI trained on flawed data that generates systematically biased recommendations with high expressed confidence.

What Smart Data Actually Means

Smart Data is not the opposite of Big Data, and it is not a strategy built on collecting less information. Smart Data is the philosophy of making data usable, trustworthy, and directly aligned with the specific decisions and outcomes it needs to support — before worrying about scale and volume.

The critical conceptual shift between Big Data and Smart Data is the question you start with:

Big Data asks: “How do we collect and store as much data as possible and find insights in it later?”

Smart Data asks: “What specific decisions do we need to make better — and what is the minimum complete, accurate, timely data required to make them?”

For a wealth management firm or family office, the Smart Data questions are highly specific: What data do our portfolio managers need at 8:00am to make today’s allocation decisions — and is that data validated before they open their systems? What data does our risk function need in real time — and is it arriving with sub-second latency or a 30-minute lag? What data do our compliance teams need for this week’s regulatory filings — and is it in the format the regulator requires?

Smart Data answers these questions before building infrastructure. It defines exactly which data is needed, for which purpose, at what quality standard, and at what delivery speed — and then builds a pipeline that reliably delivers precisely that. Everything else is noise.

The Smart Data Framework: Five Core Disciplines

Capitoline’s Smart Data™ methodology — which underpins our Financial Data Management (FDM) platform — is built around five core disciplines that collectively produce data wealth management firms can actually rely on.

Discipline 1: Source Rationalisation

Most wealth management firms are paying for more data sources than they need, and failing to integrate the ones they have paid for. Smart Data begins with mapping every data source against every downstream use case — and eliminating sources that are redundant, unreliable, or not connected to any specific decision outcome. The goal is a rationalised data source architecture where every feed has a defined purpose, a defined quality standard, and a defined downstream consumer.

Discipline 2: Validation and Quality Scoring

Every data point entering a Smart Data pipeline is validated against a defined quality framework before it reaches downstream systems. This validation catches the specific failure modes that cause damage in wealth management: stale prices, missing positions, duplicate records, mis-classified instruments, incorrect counterparty assignments, and format inconsistencies between data sources. At Capitoline, this process delivers our 99.8% data quality standard across 350+ integrated sources.

Discipline 3: Normalisation and Enrichment

Raw data from different sources arrives in different formats, uses different identifiers (CUSIP vs ISIN vs Bloomberg ticker), and represents the same entity in different ways. Normalisation resolves these inconsistencies so that downstream systems receive a single, consistent representation of each data point. Enrichment adds context — mapping instruments to asset classes, sectors, and geographies; linking issuers to parent entities; appending regulatory classifications where required.

Discipline 4: Real-Time Delivery Architecture

Smart Data is not smart if it arrives 30 minutes late. Portfolio decisions, risk monitoring, and compliance functions increasingly operate in real time — and data infrastructure needs to match. This means moving away from batch processing paradigms toward streaming architectures that deliver validated, enriched data to downstream systems with sub-second latency from the source event.

Discipline 5: Lineage and Auditability

For regulatory compliance and internal governance, it is not enough to know that a number is correct. You need to demonstrate where it came from, when it arrived, how it was validated, and how it was used. Smart Data infrastructure maintains a complete data lineage trail — enabling compliance teams to answer any regulator question about any reported figure with documented precision.

Capitoline Smart Data™ in Practice — The Numbers

Capitoline’s Financial Data Management (FDM) platform applies the Smart Data framework across institutional wealth management operations — integrating over 350 data sources into a single validated, normalised, real-time pipeline that feeds portfolio management, risk, compliance, and client reporting systems simultaneously.

The result is not just cleaner data. It is a fundamentally different operational capability — one where advisors, risk managers, and compliance teams start every day with data they trust completely, rather than spending two hours reconciling discrepancies.

Big Data vs Smart Data — The Practical Comparison

For a wealth management firm evaluating its data strategy, the following comparison makes the practical difference between the two approaches concrete across the decisions that matter most every day.

| Decision Area | Big Data Approach | Smart Data Approach |

|---|---|---|

| Starting question | How do we collect more data? | What specific data does each decision require? |

| Success metric | Volume of data stored and processed | Quality, accuracy, and timeliness of data delivered |

| Portfolio valuation | Multiple pricing sources, manual reconciliation required daily | Single validated pricing feed, reconciled automatically before market open |

| Risk management | End-of-day batch risk calculations on potentially stale data | Real-time intraday VaR on validated, normalised positions with full coverage |

| Client reporting | Reports manually checked before sending due to data trust issues | Reports generated automatically from trusted data — no manual QA required |

| Compliance filing | Regulatory data assembled and checked manually, high error risk | Compliance data continuously maintained with full audit trail and automated validation |

| AI / model inputs | Models trained on unvalidated data, producing unreliable outputs | Models trained on 99.8% quality validated data — reliable, auditable outputs |

| Operational cost | 15–25% of revenue absorbed by data rework and error correction | Rework cost minimised through upstream validation and quality scoring |

What This Means for Wealth Managers and Family Offices Specifically

For Multi-Office Wealth Management Firms

If you are operating across multiple offices — each with its own advisors, client relationships, and potentially its own systems — data fragmentation is your primary data problem. Different offices using different data sources, different pricing vendors, and different formats for the same data produces a firm-wide environment that cannot be trusted or consolidated. Smart Data solves this by establishing a single validated data standard across all offices — the same pricing, the same positions, the same risk numbers — delivered from a centralised pipeline to every location simultaneously.

For Family Offices

Family offices face a specific version of the data quality problem: the assets under management are complex (real estate, private equity, alternatives, liquid securities, and often multi-generational structures), the clients are the most demanding in wealth management, and regulatory requirements are increasingly sophisticated. In this context, data quality is not just an operational nicety — it is the foundation of every client conversation. When a family member asks why their net worth figure changed by $2 million between reports, “there was a data issue” is not an acceptable answer.

For Advisors Building AI-Powered Workflows

The wealth management industry is moving rapidly toward AI-assisted portfolio management, automated rebalancing, and model-driven client communications. All of these capabilities depend entirely on the quality of the underlying data. An AI rebalancing system operating on unvalidated data will generate confident, systematic errors. A Smart Data infrastructure is not just beneficial for AI adoption — it is the prerequisite for it to work at all.

How to Diagnose Whether You Have a Smart Data Problem

Before your next data strategy review or technology procurement decision, ask your team these five diagnostic questions honestly. The answers will tell you which problem you actually have.

- How long does it take your team each morning to reconcile data discrepancies? If the answer is more than 20 minutes, you have a Smart Data problem, not a volume problem.

- When was the last time a client or auditor identified a data error before your team did? If this has happened in the last 12 months, your data quality standard is not high enough.

- Can your risk team run a full firm-wide risk calculation right now, in real time? If the answer is “we run it overnight,” your data delivery architecture is a decade behind.

- How many separate systems does your team need to open to get a complete picture of one client’s portfolio? If the answer is more than two, you have a fragmentation problem that more data volume will make worse.

- If you asked every investment team member where your pricing data comes from — would they all give the same answer? Inconsistency here is evidence of an uncontrolled, unvalidated data environment.

If you answered honestly and three or more questions revealed a problem, your data challenge is a Smart Data quality and architecture problem — and investing in more data volume before addressing it will make things worse, not better. Fix the foundation first.

The Competitive Advantage That Smart Data Creates

Beyond the risk reduction and operational efficiency arguments, there is a compelling competitive advantage case for Smart Data in the current wealth management market.

A mid-size wealth management firm with Smart Data infrastructure can now deliver family office-level reporting quality — and win business from larger, slower competitors who are still reconciling spreadsheets. The personalisation, precision, and speed that institutional clients are increasingly demanding is not possible without trusted, real-time data infrastructure underneath it.

The firms that will lead the next decade of wealth management are not necessarily those with the most data. They are the ones whose advisors walk into every client meeting with complete confidence in every number on the page. Whose risk managers see the same risk picture as the CRO, in real time. Whose compliance teams file accurate regulatory reports without a week of manual preparation. Whose AI systems produce reliable recommendations because the data they are operating on is actually correct.

That is what Smart Data delivers. And the gap between the firms that have it and the firms still investing in volume without addressing quality is widening every year.

See Smart Data™ in Action

Capitoline’s Financial Data Management platform unifies 350+ data sources into a single validated, real-time Smart Data pipeline — delivering the 99.8% data quality standard that wealth management operations depend on. Request a demonstration and see what your data infrastructure could look like.

Request a Demo Learn About FDM →Frequently Asked Questions

What is the difference between Big Data and Smart Data in wealth management?

Big Data focuses on collecting and processing maximum data volumes. Smart Data is the philosophy of making data usable, trustworthy, and aligned with specific business and investment outcomes — quality over quantity. For wealth management firms, Smart Data means curating, validating, and delivering only the data that directly improves portfolio decisions, risk management, client reporting, and compliance — not storing everything in the hope that something useful will emerge from the volume.

Why is poor data quality a problem for wealth managers and family offices?

Poor data quality leads directly to incorrect portfolio valuations, inaccurate risk calculations, compliance failures, delayed client reporting, and investment decisions based on flawed information. Research indicates that data quality issues cost financial services firms an estimated 15–25% of their operating revenue in rework, error correction, and missed opportunities. For family offices, the impact is even more acute because the clients are the most scrutinising in wealth management.

What does a Smart Data strategy look like for a wealth management firm?

A Smart Data strategy defines exactly which data points are needed for each decision — portfolio valuation, risk assessment, compliance reporting, client communication — then builds a validated pipeline that sources, validates, normalises, and delivers precisely that data. It covers five disciplines: source rationalisation, validation and quality scoring, normalisation and enrichment, real-time delivery architecture, and data lineage and auditability. Quality over volume. Real-time delivery over batch processing. Business outcomes over data storage metrics.

How does Capitoline’s Financial Data Management platform support wealth managers?

Capitoline’s FDM platform integrates 350+ data sources into a single unified Smart Data pipeline — delivering validated, normalised, real-time data to portfolio management, risk, compliance, and client reporting systems simultaneously. The platform achieves a 99.8% data quality standard through automated validation, deduplication, normalisation, and enrichment — eliminating the manual reconciliation work that consumes advisor and operations time every morning.

Is Smart Data relevant for smaller wealth management firms, or only large institutions?

Smart Data is particularly relevant for smaller and mid-size firms and family offices — because these firms are most exposed to the operational costs of poor data quality, and have the most to gain from infrastructure that eliminates manual reconciliation. Large institutions have operations teams to manually compensate for data quality failures. Smaller firms do not — which means Smart Data infrastructure delivers proportionally greater competitive and operational advantage at smaller scale.