The global investment banking industry advises on the world’s most complex financial transactions, yet frequently relies on outdated legacy technology. This article explores the root causes of this technical debt, the operational risks it creates, and the blueprint for a modern technology stack. As traditional finance converges with digital assets and high-velocity markets like U.S. power trading, modernizing infrastructure is no longer an IT initiative—it is a mandate for survival.

The Core Paradox of Investment Banking

The global investment banking sector operates on a profound irony. This industry is built entirely on guiding clients through high-stakes corporate evolutions—orchestrating multinational mergers, launching massive initial public offerings (IPOs), and structuring intricate debt. Yet, behind the cutting-edge trading floors, these same institutions often run their internal operations on technology infrastructure that their own clients would deem unacceptable.

If a modern energy conglomerate went public with the level of technical debt found in the back offices of many tier-one banks, analysts would raise immediate red flags. Legacy systems, patched together over decades of aggressive mergers and sweeping regulatory expansions, have created a sprawling web of operational risks.

The technology transformation currently underway is not a simple software update. It is a massive convergence of competitive, regulatory, and client-driven pressures forcing a structural evolution. In markets that demand absolute real-time precision—such as the highly volatile United States power and commodities trading sectors—the glaring inadequacies of legacy banking infrastructure become an existential threat.

The Genesis of Technical Debt in High Finance

To understand the current predicament, we must examine how modern mega-banks were formed. The history of banking is one of relentless consolidation.

Ideally, when one bank acquires another, the acquired data and operations migrate seamlessly into a superior technology ecosystem. In reality, this “rip-and-replace” methodology is fraught with risk, wildly expensive, and deeply disruptive.

The “Layering” Problem and Regulatory Expansion

Instead of unified integration, institutions historically opted for a layering approach. They built complex middleware—digital duct tape—to force disparate mainframes, proprietary databases, and siloed applications to communicate.

Following major financial crises, global regulators introduced sweeping mandates aimed at increasing transparency. In the U.S., frameworks dictating derivatives trading and capital requirements forced banks to rapidly build new compliance modules. Because these mandates had strict deadlines, banks built standalone applications rather than integrating them holistically. The result is a fragile ecosystem where a single transaction might pass through dozens of internal systems before it is fully cleared and reported.

The Anatomy of Operational Risk: Where Legacy Systems Fail

The legacy system problem directly impacts the bottom line, creating measurable risks across three critical areas:

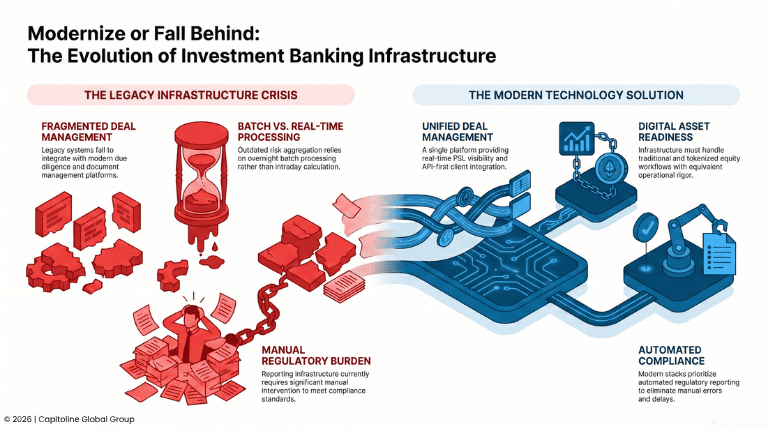

1. Fragmentation in Deal Management

A standard merger involves mountains of sensitive data: financial models, legal contracts, and due diligence reports. Legacy deal management systems operate as isolated vaults that do not integrate cleanly with modern, cloud-based platforms.

When an investment banker updates a financial model, the process is often entirely manual—downloading data from one secure room, manipulating it locally, and uploading it elsewhere. This friction creates severe operational risks:

- Poor Version Control: Decisions may be based on outdated valuation models.

- Security Vulnerabilities: Moving highly sensitive data across fragmented systems increases the surface area for potential breaches.

2. The Danger of Overnight Batch Processing in Risk Aggregation

The vulnerabilities of legacy banking technology are most glaring in risk management. Here, the parallels to U.S. power trading are highly instructive.

In the U.S. wholesale power markets (operated by RTOs like PJM, ERCOT, or CAISO), volatility is constant. Because electricity cannot be easily stored, supply and demand must balance perfectly every second. A sudden pipeline disruption can cause power prices to surge exponentially in minutes. Power traders operate in an environment where intraday, real-time visibility into their Value-at-Risk (VaR) is a fundamental prerequisite for survival.

Contrast this with traditional investment banks, which often rely on overnight batch processing. Because the bank operates on dozens of disparate systems, it is computationally too heavy to calculate total firm-wide risk in real time. Systems collect the day’s data and run massive computing batches overnight. By the time a Chief Risk Officer realizes the bank has breached its risk limits the next morning, the market has already moved, and capital is lost.

3. The Burden of Manual Regulatory Reporting

Financial authorities require highly specific reports regarding trade execution and liquidity ratios. Because legacy systems lack a “Single Source of Truth,” regulatory reporting requires significant manual intervention.

When a regulator requests a “trade reconstruction”—a comprehensive timeline of a transaction—banks often have to stitch together voice recordings, instant messages, trade blotters, and settlement systems manually. This is slow, prone to human error, and incredibly expensive.

The Squeeze: External Pressures Forcing Change

The push to abandon legacy systems is driven aggressively by external forces, making technological transformation mandatory.

- The Rise of Agile Competitors: Boutique and mid-market investment banks, built natively in the cloud, execute transactions with operational efficiency that legacy-laden peers cannot match. Simultaneously, fintech providers are offering automated syndication platforms and cross-border settlement services, competing directly for traditional banking business.

- The Client Expectation Paradigm: Corporate treasurers and institutional investors live in seamless, API-driven ecosystems. They no longer accept static, weekly PDF reports. They expect real-time interactive portals and API-first integrations that feed bank data directly into their own Enterprise Resource Planning (ERP) systems.

- Relentless Regulatory Scrutiny: Regulators are moving away from static reports, increasingly demanding direct, programmatic access to bank data to dynamically monitor systemic risk.

Blueprinting the Modern Technology Stack

Surviving this convergence of pressures requires shifting from rigid, monolithic architecture to agile, interconnected ecosystems.

System Comparison: Legacy vs. Modern Architecture

| Feature | Legacy Banking Infrastructure | Modern Technology Stack |

|---|---|---|

| Data Architecture | Siloed, proprietary databases | Unified data taxonomy (Single Source of Truth) |

| Risk Management | End-of-day / Overnight batch processing | Real-time, event-driven streaming analytics |

| Client Integration | Manual portals, static PDF reporting | API-first, programmatic ERP integration |

| Regulatory Reporting | Heavy manual reconciliation | Automated, “touchless” data extraction |

Key Pillars of the New Stack

- Unified Deal Management Platforms: Replacing disparate vaults with a singular, cloud-native platform ensures absolute version control, rigorous audit trails, and secure collaboration.

- Real-Time Risk and P&L Visibility: Utilizing event-driven architecture and message brokers allows risk engines to instantly recalculate firm-wide exposure the moment a trade is executed.

- Automated, Touchless Reporting: Smart algorithms extract necessary data and format it according to jurisdictional mandates with zero manual intervention.

- API-First Client Integration: Application Programming Interfaces (APIs) allow the bank to easily plug in best-of-breed third-party solutions and expose services directly to clients for automated workflows.

The Digital Asset Frontier: Bridging TradFi and DeFi

One of the most significant drivers of modernization is the rapid evolution of asset classes. There is an urgent need to manage traditional equity, physical commodities, and digital assets on fully integrated platforms.

As tokenized equity and crypto-adjacent financing move from experimental to operational, the divide between Traditional Finance (TradFi) and Decentralized Finance (DeFi) is collapsing.

The Mechanics of Tokenization in Energy Markets

Tokenization involves representing ownership of a real-world asset as a digital token on a blockchain. In the U.S. energy and power sectors, this holds massive potential.

Consider the financing of a utility-scale solar facility or the trading of Renewable Energy Certificates (RECs). By tokenizing the equity in that infrastructure or future Power Purchase Agreements (PPAs), banks can:

- Fractionalize ownership to increase liquidity.

- Automate the distribution of dividends or energy credits via smart contracts.

The Infrastructure Imperative

Distributed Ledger Technology (DLT) operates on real-time, immutable settlement. If a bank attempts to handle digital assets on a segregated system bolted onto legacy infrastructure, it is simply recreating the technical debt of the past.

Unified infrastructure is the strategic imperative. The technology must handle traditional equities, complex power derivatives, and tokenized digital assets with equivalent rigor. Smart contracts can facilitate atomic settlement—where the exchange of an asset and payment occurs simultaneously—but only if the internal architecture is capable of processing transactions in real time.

Conclusion: The Compounding Advantage of Early Adopters

The transformation of investment banking infrastructure is an arduous, capital-intensive process requiring complex change management. However, technology in financial services acts as a compounding force.

While legacy banks pay ongoing “interest” on their technical debt through operational errors and lost opportunities, early adopters are reaping a “technological dividend.” Firms that transition to unified deal management, real-time risk calculation, and API-first ecosystems can deploy code globally in days and seamlessly integrate new asset classes to capture early market share.

The institutions moving decisively now are transforming their operations from a center of friction into a distinct competitive advantage. In an industry where markets move at the speed of light, running tomorrow’s transactions on yesterday’s infrastructure is a direct path to obsolescence.