The quality of a trading decision is constrained by the quality of the information that decision is based on. In commodity markets, where real-time price movements, volatility, and liquidity conditions are constantly shifting, the difference between a trading operation that consistently extracts value and one that struggles often comes down to a deceptively simple variable: how effectively they extract tradable signals from the noise of real-time market data.

Most traders have access to the same data feeds. Bloomberg terminals, market data vendors, exchange connections – these are commoditized infrastructure that any serious trading operation can access. The differentiation comes in how that raw data is processed, validated, analyzed, and converted into actionable trading signals that can be executed with confidence.

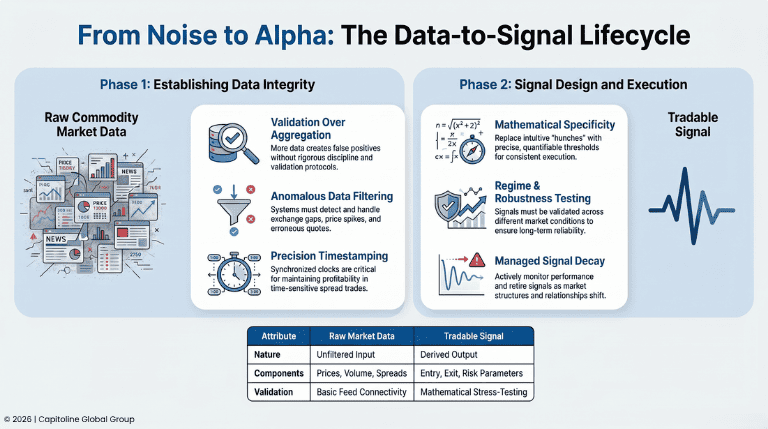

For many years, the consensus in trading technology has been that you should aggregate as much data as possible, apply sophisticated statistical methods, and hope that signal emerges from the noise. This approach produces impressive backtests but frequently fails on live markets. The reason is structural: more data doesn’t automatically produce better signals. Without rigorous signal design and data quality discipline, more data often produces more convincing false positives.

THE STRUCTURAL DIFFERENCE BETWEEN DATA AND SIGNALS

The conceptual gap between “having real-time market data” and “having tradable signals” is larger than many traders appreciate. Market data is the raw input – prices, volumes, bid-ask spreads, implied volatility, open interest. A trading signal is a derived output: a specific, testable assertion about an actionable opportunity with defined entry, exit, and risk parameters.

The conversion from data to signal requires discipline at multiple levels. First, data validation: ensuring that the real-time prices and volumes you’re receiving are accurate, that they haven’t been corrupted by transmission errors or exchange reporting anomalies, and that they reflect genuine market activity rather than spurious trades that will be busted. In commodity markets, where data latency, feed interruptions, and occasional erroneous quotes are facts of life, data validation becomes a prerequisites to signal generation, not an afterthought.

Second, signal design: specifying exactly what market conditions would constitute a trading opportunity, with mathematical precision. A signal that “looks good” intuitively rarely translates to consistent profitability. Signals that have been stress-tested against historical data, validated across market regimes, and evaluated for robustness to parameter variations are orders of magnitude more reliable than signals that are intuitive or theoretically appealing.

Third, execution discipline: having systems and protocols in place to execute signals consistently and without hesitation once they’ve triggered. The gap between a profitable signal in backtests and a profitable trading operation is often the ability to execute the signal repeatedly and systematically, even when market conditions are stressful or when prior trades from the signal have lost money.

THE DATA QUALITY IMPERATIVE IN REAL-TIME TRADING

The first challenge in real-time signal extraction is data quality. In a perfect world, real-time market data would be perfectly accurate, instantaneously delivered, and never subject to gaps or corruptions. Real markets don’t work that way.

Exchange connectivity failures cause temporary data gaps. A market data feed might drop for 30 seconds – long enough to miss significant price movements. The challenge is that if you don’t detect the gap, your signal extraction systems might miss the price move entirely, leaving you out of a trade. If you do detect the gap but don’t handle it properly, you might execute on stale data or incorrect assumptions about what happened during the gap.

Erroneous quotes and trades happen regularly. A trader accidentally enters a bid-offer order that trades at an unrealistic price. The exchange busts the trade, but the price spike happened. If your signal systems saw the spike and reacted to it, you’ve been punished for moving on false information. Successful signal extraction requires resilience against these events – recognizing them as anomalies and not treating them as genuine market moves.

Timestamp synchronization becomes critical when signals depend on the relative timing of events across multiple markets. If your clock is 200 milliseconds behind the exchange’s clock, spread trades that should be profitable at the moment they appear might be unprofitable by the time they execute. Getting timestamps right is a technical requirement that often gets overlooked until it causes problems.

Data validation systems should continuously monitor incoming real-time data for anomalies: prices that move more than historical volatility would suggest, volumes that spike far beyond normal levels, bid-ask spreads that widen to nonsensical levels. These flags should trigger investigation – either automated or manual – before signals based on questionable data get executed.

THE SIGNAL DESIGN PROCESS

Once data quality is assured, the next step is signal design. This is where the intellectual work of trading happens, and it’s also where many trading operations go wrong. The design process needs to balance several competing objectives: specificity (the signal should be mathematically precise and unambiguous), robustness (it should work across different market conditions and time periods), and feasibility (it should be executable with reasonable slippage and transaction costs).

The typical workflow for signal design begins with a hypothesis: a specific market condition or price relationship that you believe creates a tradable opportunity. In commodity markets, examples might include:

An inversion in the oil futures curve – when near-term contracts trade at a premium to future contracts, despite the usual pattern being contango. This can signal tight near-term supply conditions and creates an opportunity to profit from mean reversion as the curve normalizes.

A divergence between natural gas prices and heating degree days. Heating demand should drive natural gas prices, but sometimes prices move independent of weather forecasts. When the divergence is large, it suggests a trading opportunity as prices revert to reflecting actual thermal demand.

A relationship between crude oil prices and the broad equity market. Historically, energy prices and equity prices move together during demand shocks but diverge during supply shocks. Identifying which regime you’re in, and positioning accordingly, is a consistent source of trading signals.

For each hypothesis, the next step is quantification: defining exactly what numbers constitute the signal. Rather than “the curve looks inverted,” it becomes “when the price of the front-month contract exceeds the three-month contract by more than $0.50 per barrel, that’s a signal.” This specificity is essential for backtesting and for ensuring that the signal will execute consistently.

The backtesting process applies the signal to historical data and measures how it would have performed. The key requirement is honesty about backtesting. Walk-forward testing (testing on data the signal was designed on, then validating on separate data) is essential. Optimization bias (tuning the signal parameters to fit historical data) is a constant danger – a signal that works perfectly on historical data but fails on new data is worthless.

Parameter robustness is worth checking explicitly. If your signal’s profitability depends on a threshold being exactly $0.50 and it falls apart if the threshold is $0.45 or $0.55, the signal isn’t robust. If it performs across a range of thresholds – $0.40 to $0.60 – then you have a signal worth trading.

Regime testing is critical. Does the signal work in trending markets and ranging markets? Does it work when volatility is low and when volatility is elevated? Does it work in periods of tight credit and periods of loose credit? A signal that only works in specific market regimes is a vulnerability, not an advantage, because markets don’t stay in any single regime.

CONVERTING SIGNALS TO EXECUTABLE ORDERS

Once signals are designed and validated, they need to be operationalized. This means building systems that monitor real-time market conditions, detect when signal conditions are met, and execute trades consistently and without manual intervention.

The execution layer needs to be disciplined about the order of operations. First, confirm that the signal condition is genuinely met (not a data glitch). Second, check risk limits to ensure the trade fits within portfolio constraints. Third, size the position appropriately based on current market liquidity and the portfolio’s risk budget. Fourth, submit the order to the market. Fifth, monitor the execution to confirm it happened as expected.

This sounds straightforward, but each step has practical complexities. Signal confirmation requires distinguishing between a genuine signal and a data anomaly not always obvious in real time. Risk checks need to account not just for the position being added but for how it interacts with existing positions. Position sizing in illiquid markets requires estimating impact costs, not just using a theoretical optimal size.

THE COMPETITIVE REALITY OF SIGNAL QUALITY

The most successful commodity trading operations treat signal quality as a core competitive variable. They invest in data infrastructure and validation. They spend time designing and testing signals. They monitor signal performance on live trades and adjust when signals drift from their backtested behavior.

They also understand that signal decay is inevitable. A signal that works consistently for two years will eventually stop working as market structure changes, other traders discover the same pattern, or the underlying market relationship that generated the signal shifts. Successful operations have processes for identifying when a signal has decayed and retiring it before it becomes a source of losses.

The timeline for this business is compressed. Trading operations that are still executing on intuitive hunches or hand-coded spreadsheet-based signals are increasingly competing against operations that have systematized signal generation and execution. The gap in profitability between these approaches is real and growing.

BUILDING THE INFRASTRUCTURE FOUNDATION

Supporting high-quality signal extraction at scale requires infrastructure that most trading operations don’t have naturally. Real-time data pipelines that deliver market data with minimal latency. Calculation engines that can evaluate complex signal logic on thousands of symbols every second. Execution systems that can translate signal outputs into market orders. Monitoring and alert systems that flag when signals aren’t performing as expected.

The build-versus-buy decision is strategically important. Building this infrastructure from scratch is a multi-year, capital-intensive process. Partnering with providers that have already built the infrastructure allows trading operations to focus on the highest-value work: signal design and trading logic.