Portfolio risk measurement has become materially more complex over the past decade. A generation ago, portfolio risk analysis meant understanding equity volatility and bond duration. Today, institutional portfolios span equities, fixed income, alternatives including real estate and private equity, commodities, and increasingly, digital assets. Each has its own risk characteristics, liquidity profile, return distribution, and correlation structure. Measuring coherent risk across all of these simultaneously is a problem that many portfolio managers and risk officers have only begun to engage seriously.

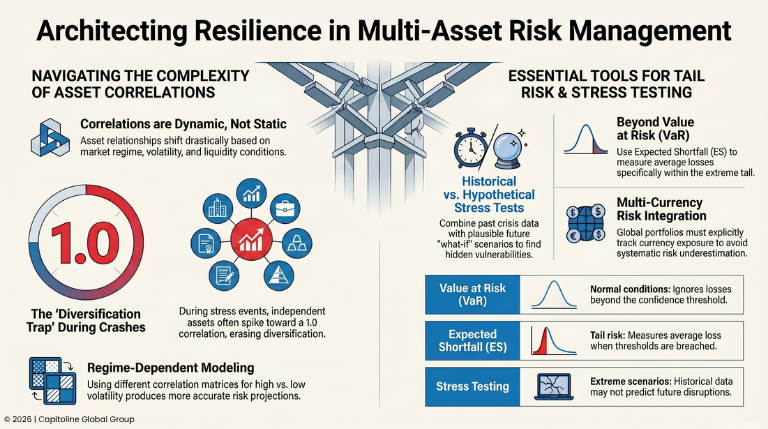

The complexity is compounded by the fact that correlations between assets are not static. They shift depending on market regime, volatility environment, and liquidity conditions. The correlations that govern portfolio behavior during normal market conditions are often different from those that govern behavior during stress events. A portfolio that looks adequately diversified under normal correlations can lose that diversification and become dangerously concentrated during periods when correlation structures break down.

Professional investors who manage coherent risk across multiple asset classes have built infrastructure and processes that reflect this complexity. Understanding how they do it—and why it matters—is essential for any institution managing assets seriously.

THE CORRELATION REALITY ACROSS ASSET CLASSES

The first structural challenge in multi-asset risk aggregation is correlation modeling. Traditional portfolio theory assumes correlations are constant or predictable. They aren’t. Correlations between equities and bonds shift dramatically depending on whether the market is concerned about growth or inflation. Correlations between commodities and equities reverse between periods when commodities are driven by growth expectations versus periods when they’re driven by dollar movements.

The most damaging correlation breakdowns happen during stress events. Correlations between assets that normally move independently tend to spike sharply as investors reduce exposure across the board. A portfolio that is 60% equities and 40% bonds, with low historical correlation, might experience correlation approaching 1.0 during a market crash—meaning both components fall together, providing no diversification benefit precisely when it’s most needed.

Modeling this requires more sophisticated approaches than assuming correlations are constant. The most rigorous risk frameworks use regime-dependent correlations: different correlation matrices for different market conditions (high volatility versus low volatility, growth scares versus inflation concerns, periods of liquidity abundance versus periods of stress). This requires identifying regimes from market data and associating each regime with its specific correlation structure.

Dynamic correlation models that update based on recent market movements provide an intermediate approach. They’re more responsive than static correlations but less computationally intensive than full regime-switching models. For many applications, they provide a practical balance between accuracy and tractability.

THE CHALLENGE OF MULTI-CURRENCY EXPOSURE

For global portfolios, currency exposure creates a second layer of correlation complexity. Assets across different currencies don’t move independently of currency rates. A US-based investor with a European equity position has exposure to both European equity returns and EUR/USD movements. During periods when the dollar strengthens, even well-performing European equities might generate negative returns for US investors.

The strategic question for portfolio managers is whether to hedge currency exposure or leave it unhedged. The answer depends on the investor’s view on currency movements, the overall portfolio’s currency exposure, and the cost of hedging.

From a risk measurement perspective, the question is how to properly account for currency exposure in portfolio risk calculations. A calculation that ignores currency exposure will systematically underestimate risk for global portfolios. One that hedges all currency exposure might overestimate cost without providing proportional risk reduction. The correct approach depends on the specific portfolio’s currency exposures and the investor’s strategy.

The Risk Management Systems that handle this properly track currency exposure explicitly, calculate risk both as reported in local currency and as reported to the investor’s base currency, and allow for strategic currency hedging decisions.

STRESS TESTING AND SCENARIO ANALYSIS

The most important discipline in multi-asset risk management is stress testing: evaluating how a portfolio would perform under adverse market conditions that haven’t yet occurred but plausibly could.

The standard approach is to identify historical stress periods—the 2008 financial crisis, the 2011 sovereign debt crisis, the 2020 COVID crash—and evaluate how the current portfolio would have performed during those periods. This establishes bounds on losses that a reasonable worst-case might produce.

The limitation of historical stress testing is that it’s anchored to events that happened. If a portfolio is designed to avoid the risks that materialized during past stress events, it might be vulnerable to entirely different stresses that haven’t yet occurred.

Hypothetical stress scenarios complement historical analysis. These are plausible-but-haven’t-happened scenarios: a sharp increase in interest rates, a major geopolitical disruption, a commodity supply shock, a severe credit event, etc. For each scenario, risk managers specify what would happen to key market variables and calculate how the portfolio would respond.

A well-designed stress scenario is detailed and internally consistent. If interest rates rise sharply, what happens to equity valuations, currency movements, credit spreads? The scenario needs to reflect the actual cross-market relationships that would characterize that stress, not an arbitrary collection of market moves.

The challenge in designing stress scenarios is distinguishing between scenarios that are plausible and those that are so extreme they’re effectively impossible. A scenario where equities fall 50%, bonds fall 40%, and credit spreads widen 500 basis points simultaneously might happen in a genuine catastrophe, but it’s sufficiently implausible that planning around it—at the cost of reducing expected returns—isn’t reasonable risk management.

VALUE AT RISK AND TAIL RISK MEASUREMENT

Value at Risk (VaR) is a standard portfolio risk metric: the maximum loss expected under normal conditions at a given confidence level. A 95% one-day VaR of $500,000 means that under normal market conditions, there’s a 95% probability that the portfolio won’t lose more than $500,000 in a single day.

VaR has well-known limitations. It doesn’t measure losses that occur in the tail beyond the confidence threshold. A portfolio with a 95% VaR of $500k might experience $2 million losses in the 1% of days when stress occurs. VaR also depends heavily on the volatility model used to calculate it, making it sensitive to parameter choices.

Expected Shortfall (ES) addresses some of these limitations by measuring the average loss conditional on losses exceeding the VaR threshold. It captures tail risk more directly than VaR and is less subject to parameter sensitivity.

For multi-asset portfolios, the most important use of risk metrics like VaR and ES is not as precise point estimates but as decision tools. They provide a framework for thinking about risk in quantitative terms and for comparing risk across different portfolios or strategies. The specific numerical output matters less than the discipline of regularly calculating and reviewing these metrics.

THE IMPLEMENTATION CHALLENGE

Building and maintaining multi-asset risk infrastructure is complex. It requires data infrastructure that consolidates positions from multiple trading systems, custody reports, and external sources. It requires calculation engines that can evaluate complex risk models on portfolios with thousands of positions across multiple asset classes. It requires governance processes that define whose positions are included, how they’re validated, and how discrepancies are resolved.

Many institutions struggle with this because they’ve accumulated risk systems over years of acquisitions, business expansion, and technology changes. The result is often multiple systems of record: equities positions in one system, fixed income in another, alternatives in a third. Reconciling these into a single coherent risk view requires significant effort.

The firms that have built coherent multi-asset risk frameworks have typically made a strategic decision to prioritize this infrastructure investment despite the cost and complexity. The benefit is that they can manage genuinely coherent risk across their portfolio and avoid the surprises that come from data gaps and siloed systems.